16 min Read

16 min Read January 3, 2025

January 3, 2025Picture this: You’re a cunning money launderer who is plotting your next move to launder money within the United States. What would you go for?

Banks? Too risky. They are closely watched.

Broker-dealers? No chance; their AML compliance is airtight.

Mutual funds? Forget it; they’re already in the crosshairs.

Then, you spot the perfect loophole: investment advisers.

Investment advisors operate without strict AML obligations; they handle vast sums of money with minimal oversight. It’s a dream scenario for anyone seeking to slip illicit funds under the radar.

For years, investment advisers operated in a regulatory gray zone. They handled massive wealth without formal AML oversight. FinCEN AML rule finally brings them into the fold.

Financial Crimes Enforcement Network

Financial Crimes Enforcement Network (FinCEN) recently introduced a new Anti-Money Laundering (AML) rule. It is aimed at closing gaps in the regulatory framework to strengthen the U.S. financial system against money laundering and terrorist financing.

Investment advisers, who were previously exempt from certain AML regulations, are now in the spotlight. But what has pushed FinCEN to take such a drastic step and why now? Was this an abrupt response, or was this a long-overdue rule?

The New Rule in the Making: Backstory of FinCEN New Law 2024

In 2018, the U.S. authorities discovered a sophisticated money laundering scheme that spanned continents and industries. At its center was a famous, high-net-worth individual who exploited a relatively blind spot in the regulatory framework: the investment advisors.

He was able to launder millions of dollars from illicit activities using an elaborate network of shell companies and offshore accounts. The individual had enlisted the help of a reputable investment adviser to manage their assets. Without suspicion, the adviser facilitated investments in real estate, private equity, and high-value art.

On the surface, these transactions appeared legitimate and were backed by a facade of well-established documents. The investment adviser was operating outside the purview of strict AML oversight. He thus unknowingly became a key player in layering and integrating the illicit funds into the legal financial system.

By the time red flags were raised, the launderer had successfully funneled millions into untraceable investments. But this was just the tip of the iceberg. In recent years, many similar cases have come to the surface, highlighting the need for a new FinCEN AML rule.

Now, we finally have it. So what is it about, and how will it impact the regulatory industry?

What is the New FinCEN AML Rule?

The New FinCEN rule, under the Bank Secrecy Act (BSA), effective January 2026, has categorized many registered investment advisors and Exempt reporting advisors as financial institutions who are now required to follow AML requirements.

Here’s what these entities are supposed to do- moving forward:

1. Develop and implement AML programs: These programs must be tailored to the risks the adviser faces. They should also be aligned with FinCEN regulations.

2.File Suspicious Activity Reports (SARs): Advisers must monitor client activities and transactions. Additionally, they should report suspicious behaviors to FinCEN.

3.Comply with record-keeping and reporting requirements: Advisers must maintain detailed records of financial transactions.

4.Collaborate with financial institutions: Advisers must share information with banks and other entities to prevent money laundering schemes.

Decoding the AML Rules: Who’s In and Who’s Out?

The Advisers Act defines an investment adviser as “a person or firm that, for compensation, is engaged in the business of providing advice to others or issuing reports or analyses regarding securities.”

The final rule will cast a wide net and will cover a range of entities that are operating as investment advisors. It specifically includes legal entities, individuals, or trusts that are registered with the Securities and Exchange Commission (SEC) under Section 203 of the Investment Advisers Act of 1940.

Here’s a breakdown of who falls under its scope:

- General Partners: SEC-registered investment advisers and those exempt from SEC reporting.

- Affiliated Managers: Managers affiliated with SEC-registered entities.

- Venture Capital Fund Advisers: Professionals advising on venture capital investments.

- Private Fund Advisers: These advisers, regardless of their registration status or geographic location, are also included.

However, certain entities are excluded from the rule. They include

- Mid-sized and multi-state advisers

- Advisers without assets under management

- Pension consultants

Why? Because these exclusions recognize the relatively lower financial crime risks associated with such entities.

Why FinCEN Had to Step In: The Need for the Rule

Investment advisors play an important role in the financial ecosystem. They not only guide clients in managing large amounts of money but are also involved in complex transactions across multiple sectors, such as the securities market, real estate, and private equity.

Due to their large influence, they are considered as important gatekeepers against money laundering. There are two main ways in which investment advisors can contribute to money laundering. They can either be exploited by bad actors, or they can themselves act as bad actors who facilitate crime.

In the infamous Bernie Madoff Ponzi scheme, many financial advisers and institutions unknowingly facilitated Madoff’s fraudulent activities by recommending his investment products to their clients. Although the advisors were not guilty of intentional wrongdoing, their negligence made them complicit in the crime.

Similarly, in a 2024 case involving Jeffrey Slothower, former registered investment adviser and founder of Battery Private, he was convicted of wire fraud, investment adviser fraud, and money laundering. He misappropriated over $1 million from his clients and spent that money on luxury items.

These cases emphasize the need for FinCEN’s new rule, which not only ensures investment advisers are regulated but also helps prevent bad actors from exploiting gaps in the system. But that is not all.

In a comprehensive document by the US Financial Crimes Enforcement Network, investment advisers have been used to launder illicit proceeds from corruption, fraud, and tax evasion, including funds controlled by sanctioned entities like Russian oligarchs.

Additionally, foreign states like China and Russia exploit advisers for access to critical technology. These issues underscore the need for FinCEN’s new rule to enhance oversight.

Why Were Investment Advisers Previously Overlooked?

Before the rule, investment advisers were not considered primary channels for illicit money due to their advisory (non-execution) role. However, as their influence and market involvement has grown, so has the recognition of the risks they pose in facilitating:

- Complex layering of illicit funds across multiple jurisdictions.

- Concealment of illegal wealth through legitimate-looking portfolios.

AML Responsibilities of Investment Advisers under FinCEN’s rule

Given their responsibilities, investment advisors are important in detecting and preventing money laundering. Under the rule, their new responsibilities will include

1. Client Screening under KYC

Advisors need to verify their client’s identity and assess their financial profiles for any unexplained wealth or inconsistent transaction history.

2. Monitoring Transactions

Advisors also need to track how various funds are allocated. They are supposed to look for any suspicious patterns. These can be abrupt changes in investment amounts or high-frequency transactions without clear economic justification.

3. Reporting of Suspicious Activity

If advisers identify irregularities, they are required to file SARs with FinCEN. For example, a client suddenly moves funds offshore, or an investment vehicle shows connections to politically exposed persons (PEPs) or sanctioned entities.

4. Collaboration with Financial Institutions

Advisers often act as liaisons between their clients and other institutions (e.g., banks and brokers). This position allows them to share crucial information with these entities to combat laundering efforts.

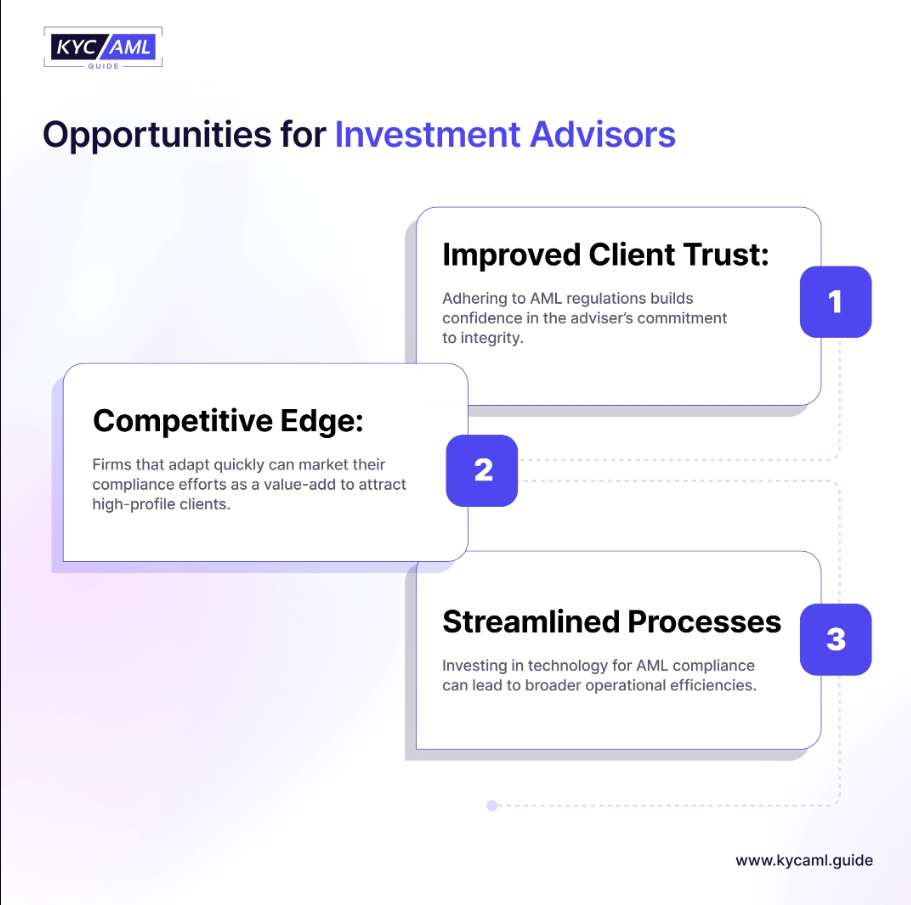

What does the Rule mean for Investment Advisers?

The new FinCEN AML rule is going to change how investment advisors conduct their business. The ones who will comply soon with the new status quo will be more likely to remain relevant in the long run.

Here is how the new rule will impact advisors:

1. Recordkeeping and Travel Rules: Investment advisers must keep detailed records related to the transfer of funds, ensuring traceability and compliance with the BSA. These records support the identification of illicit financial activity.

2. Media Searches and Screening: FinCEN advises that investment advisers aren’t categorically required to perform media searches or screenings for all clients but should apply risk-based monitoring. For higher-risk clients, advisers may need additional information to monitor changes and external developments effectively.

3. Information Sharing: Advisers are required to actively share information with FinCEN, law enforcement, government agencies, and other financial institutions. This will enhance collaboration to detect and combat financial crimes.

4. SAR and CTR Filing: They must file Suspicious Activity Reports for transactions deemed suspicious. Additionally, they are obligated to submit Currency Transaction Reports (CTRs) for cash transactions exceeding $10,000 unless exempted.

5. Customer Identification Programs (CIPs): Investment advisers need to establish robust Customer Identification Program that identify and verify customers using risk-based procedures. They must collect identifying details such as names, dates of birth, addresses, and ID numbers.

6. AML Exemptions for Mutual Funds: Advisers can exclude mutual funds with their own compliant AML programs from SAR and AML filing obligations. This will help streamline processes while maintaining oversight.

7. Transaction Monitoring: FinCEN clarifies that investment advisers are not required to use automated transaction monitoring systems. Instead, their monitoring should align with their risk profile and rely on reasonable internal controls.

FinCEN Requirements for Real Estate Under the New AML Rule

FinCEN’s new AML rule aims to combat illegal activities like money laundering and technology misuse in real estate transactions. This differs from CFIUS, which evaluates lawful foreign investments to address national security concerns.

FinCEN concentrates its AML/CFT efforts on advisers managing real estate-focused funds rather than targeting specific customers or services. Real estate investment funds with an adviser involved are already tied to BSA-defined financial institutions.

A separate FinCEN proposal requires reporting buyer and seller details for certain residential real estate transactions. These measures are expected to lower risks associated with real estate-focused funds, such as money laundering or corruption.

As a result, FinCEN decided not to explicitly include real estate-focused investment activities in the final rule.

Limited Scope of the FinCEN rule: Why is it different from the Proposed Changes?

Contrary to what everyone thought, the new rule is not as exhaustive. It is narrower than initially proposed. There are some exclusions that are discussed below.

No due diligence for Mutual Funds & Non-Advisory Roles like board positions.

Investment advisers must file SARs for red flags but aren’t required to conduct extra due diligence on portfolio companies.

Advisers must file CTRs for cash transactions over $10,000 and keep records for transfers over $3,000 unless dealing with qualified custodians already covered by AML regulations.

Conclusion

In conclusion, the new FinCEN AML rule is an important step in strengthening the financial ecosystem. It will close regulatory gaps and ensure that investment advisers are held to the same standards as other financial entities.

Moreover, for investment advisers, swift adherence to these new requirements will not only help streamline their operations but also position them as trustworthy players in a more secure financial landscape. Early compliance will ensure they stay ahead of regulatory demands, safeguarding their clients and their business reputation.

Share

Belal possess over 8 years experience in the KYC Identity Verification industry. He has consulted KYC solutions for over 20 new economy companies at DIFC and ADGM while ensuring a seamless technical integration and helped in jurisdictional compliance audits.

Table of Contents

- Financial Crimes Enforcement Network

- The New Rule in the Making: Backstory of FinCEN New Law 2024

- What is the New FinCEN AML Rule?

- Why Were Investment Advisers Previously Overlooked?

- AML Responsibilities of Investment Advisers under FinCEN’s rule

- What does the Rule mean for Investment Advisers?

- FinCEN Requirements for Real Estate Under the New AML Rule

- Limited Scope of the FinCEN rule: Why is it different from the Proposed Changes?

- Conclusion