10 min Read

10 min Read August 29, 2024

August 29, 2024While the fight against money laundering has evolved over the years, significant changes affect current laws. The Bank Secrecy Act required financial institutions to keep records and report suspicious activity. Following the 9/11 attacks, the USA Patriot Act was enacted in 2001, expanding anti-money laundering measures to combat terrorist financing. This legislation enhanced existing anti-money laundering legislation by increasing the accountability of financial institutions, including stricter recordkeeping and reporting requirements. Below is a timeline of a few national and international AML/CFT money laundering regimes.

Comparison between Money Laundering & Terrorist Financing

Let’s take a look at the differences between money laundering & terrorist financing

| Money Laundering | Terrorist Financing | |

| Purpose | To make illegal money look legitimate. | To fund terrorism and terrorist groups. |

| Source of Funds | Criminal activities | Illegal and legal activities include donations, employment, or crime. |

| Methods | Involves complex transactions using real estate, shell companies, offshore accounts, and banking secrecy havens. | Uses various methods, including formal banking, informal value transfer systems, smuggling cash or precious metals, and more. |

| Examples | Complex transactions with front companies like cash-heavy businesses, often in secrecy havens. | Ranging from buying weapons to renting vehicles, using formal banks to smuggling. |

| Detection | Suspicious transactions, like deposits, don’t match a customer’s wealth or usual activity. | Suspicious relationships, like transactions between unrelated parties. |

The various techniques used in money laundering and terrorist financing are very similar. However, there are specific methods used in terrorist financing. The table below shows some specific and common types of money laundering and terrorist financing.

What is AML CFT Compliance?

AML/CFT refers to the legal rules, procedures, and policies that financial institutions must use to detect and prevent money laundering and terrorist financing. AML/CFT compliance is important for obliged entities because it helps prevent financial crime, reduces the risk of non-compliance with national and international sanctions, and protects business reputation.

Global AML/CFT regulations are largely formulated by international bodies such as the Financial Action Task Force (FATF). The FATF Recommendations include countermeasures, transparency requirements, and standards for international cooperation in combating money laundering and terrorist financing worldwide. Other regulatory bodies to combat financial crimes are

- Financial Crimes Enforcement Network (FinCEN) in the United States

- Financial Conduct Authority (FCA) in the UK

- Monetary Authority of Singapore (MAS)

States should require financial institutions and designated non-financial businesses and professionals (DNFBPs) to mitigate, assess, and reduce money laundering, terrorist financing, and proliferation financing risks. Failure to comply with AML/CFT standards can have serious consequences, including penalties and reputational damage.

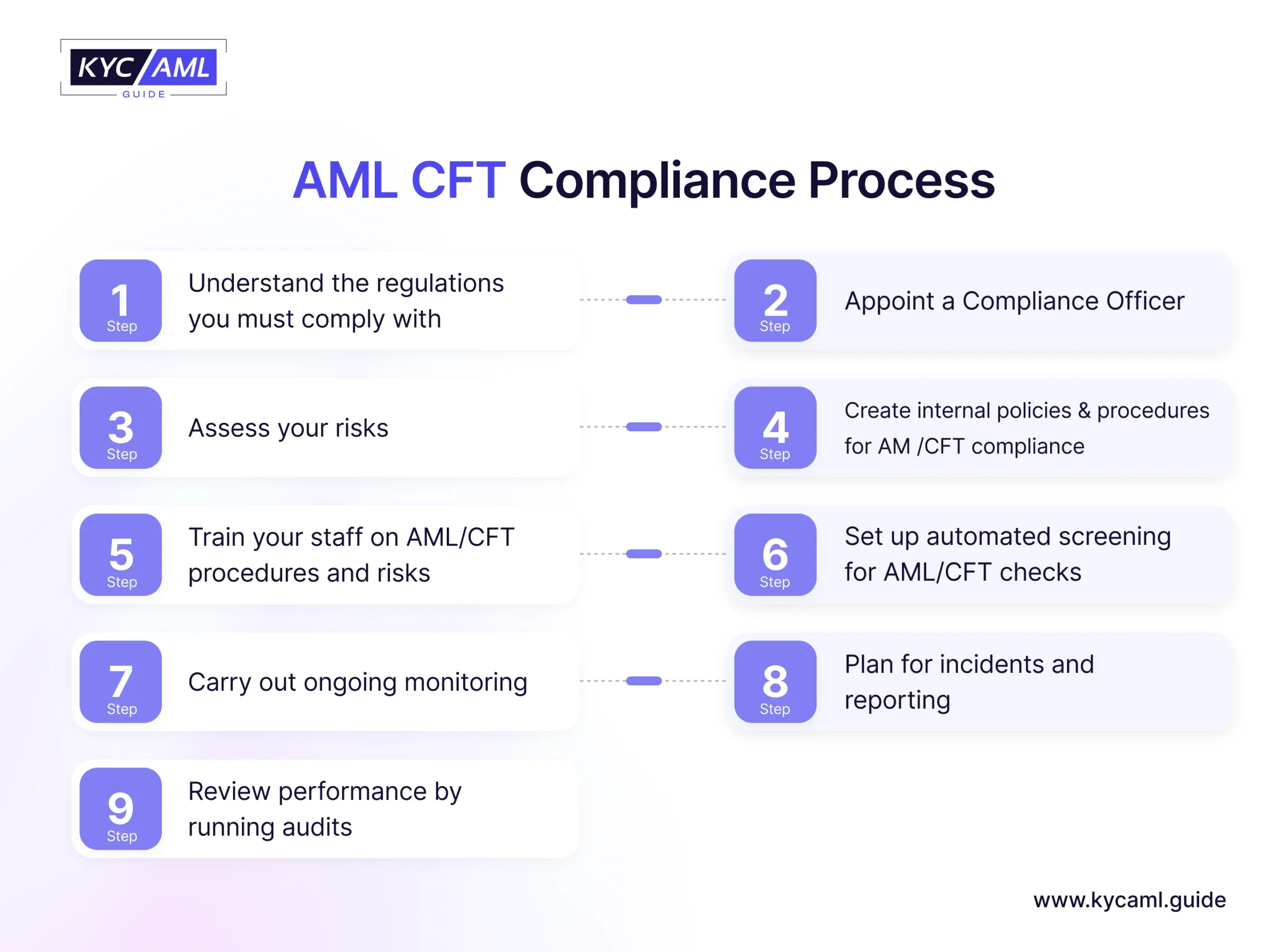

AML CFT Compliance Process

1. Understand the Regulations

To set up effective AML/CFT compliance, first understand the laws in your country. Apart from financial institutions, even Designated Non-Financial Businesses (DNFBPs) are often required to comply with AML CFT regulations due to their vulnerability to financial crimes. This includes professionals in sectors like accounting, legal, and real estate, where the risk of money laundering and financial misconduct is significant. Each region has different requirements, so don’t assume what’s true in one place applies to another.

2. Appoint Compliance Professionals

Hire skilled professionals who know the regulations to build a strong AML/CFT program. These experts help solve issues quickly, reducing risk. Implement a comprehensive training and awareness program for all employees on AML/CFT to help them identify and respond to potential risks effectively.

3. Risk Assessment

Know your organization’s risk level and manage it with the right strategies. Identify the high-risk products, services, and customer segments within your business, and prioritize your due diligence efforts accordingly. Consider factors like customer types, past transactions, and geographic location to understand the scope of risk.

4. Create Internal Policies and Procedures

Develop clear reporting frameworks for internal and external use. These must address specific

business risks and align with local and global anti-money laundering laws. Anti-Money Laundering compliance practices should include customer due diligence (CDD), know your customer (KYC) requirements, transaction monitoring, suspicious activity reporting (SAR), and record-keeping.

5. Ongoing Monitoring

Regularly check and test compliance plans to stay ahead of white-collar criminals. Consistent

reviews ensure the plan remains effective and current with any change.

AML/CFT Compliance Challenges

AML and CFT are closely related to the fight against financial crime however they have some distinct challenges.

AML focuses on identifying and stopping activities that make illegal money appear legal. The detection is sometimes difficult due to complex schemes involving multiple jurisdictions and sophisticated methods used by money launderers. CFT, however, targets disrupting the flow of funds to terrorist groups, dealing with both illicit and legitimate income sources. Since transactions may not initially appear suspicious, this makes detection challenging. Detection is challenging due to the often small sums involved and the transactions appearing to be legitimate.

Both AML and CFT need strong compliance programs, but their strategies differ: AML tracks financial transactions, while CFT focuses on intelligence and law enforcement collaboration.

RegTech tools are essential for organizations trying to comply with AML/CFT regulations. This advanced technology helps streamline the compliance process by automating tasks such as CDD, transaction monitoring, and risk assessment. It also addresses many of the challenges that organizations face in AML/CFT compliance. Compliance officers without automated tools often struggle to properly screen each customer, leading to the risk of either off-boarding valuable clients or missing out on potential red flags. Manual compliance processes can be incredibly time-consuming, making it difficult for teams to keep up with the amount of business data and speed needed to work. By implementing RegTech, businesses can analyze large data quickly, identify suspicious activity, and ensure proper compliance with regulatory requirements. This not only reduces the burden on compliance teams but also improves the consistency and effectiveness of AML/CFT efforts throughout the organization.

How can the KYC AML Guide help in AML CFT Compliance?

The KYC AML Guide can help businesses with AML and CFT compliance by offering practical advice and resources for choosing the best KYC solutions. It provides detailed vendor analysis, connects businesses with compliance services, and offers updates on the latest trends. This ensures effective customer onboarding and identity verification, reducing the risks of money laundering and terrorist financing.

Share

Muhammed Abd'al Bari is a certified Research Professional of KYC AML Guide. Connect with Muhammed on Linkedin